Growth Hacking Course

The SaaSpocalypse Is Real. It's Also Mostly Wrong.

By

February 20, 2026

Last updated: 2026-04-06

$285 billion wiped from software stocks in 48 hours. Jefferies coined "SaaSpocalypse." Retool published data showing 35% of enterprises have already replaced at least one SaaS tool with a custom build. 78% plan to build more this year.

If you're a revenue leader right now, your LinkedIn feed is basically a funeral procession for the entire software industry.

Some of it is warranted. Most of it isn't. The market is painting with a brush so broad it's practically useless.

What I see on the ground - advising B2B companies on their go-to-market every day - doesn't match the panic. Not even close.

What's Actually Happening

Nobody I work with is trying to replace HubSpot internally. Nobody's vibe-coding their own Salesforce (despite what the headlines imply).

What is happening: folk are building narrow, specific tools for workflows that were never software to begin with. A head of marketing who built a churn prediction agent over a weekend. A team that automated a cross-functional reporting process that used to live in a shared Google Sheet. Someone who stitched together an internal dashboard for something their existing tools couldn't quite handle.

These aren't SaaS replacements. They're filling the gaps between SaaS tools - the stuff that was too niche or too custom for off-the-shelf software. The stuff that fell between the cracks because no vendor was going to build a product for your specific cross-functional workflow.

The Retool stat about 35% replacing SaaS is technically true but deeply misleading. When you dig in, the tools being replaced are things like Zapier - simple integration and automation layers. Not CRM platforms. Not analytics infrastructure. The headline says "SaaS replacement." The reality is closer to "we built a workflow that connects two things."

There is a split by company type, though. More tech-centric companies have the appetite and the folk to experiment. More conservative industries are cautious. But even the aggressive ones aren't ripping out their core stack - they're building around it.

The Three Buckets

There are three buckets that matter.

Already gone. Basic content creation, translation, desk research. AI obliterated these. The copywriting tools that were essentially wrappers around foundation models - Jasper at $49/month when Claude does the same thing at $20 - are in genuine trouble. They were early AI adopters, which means they're also the earliest to be commoditised by the very technology they built on (which is poetic, if you're them).

Same story for simple workflow and project management tools. CNBC reporters built a functioning Monday.com clone in under an hour for less than $15. SaaStr's founder built an entire AI VP of Marketing using Claude and Replit that generates daily campaign plans from four years of data. If your tool's core value is a workflow layer that organises data - moving cards from column A to column B - you're exposed.

Landing page builders are in the same boat. Their value proposition is "build pages without engineering." Vibe coding lets you build anything without engineering. One marketer used Bolt to create a campaign microsite with form, CRM, and admin dashboard - zero code, saving days of dev time. That's a direct hit on Unbounce and Instapage's reason for existing.

The pattern across all of these: if your core value is a UI layer sitting on top of something AI can now do natively, you're in trouble. The wrapper is the vulnerability. 63% of vibe coding users aren't even developers - which tells you the barrier to replacing these tools is essentially gone.

Coming, but not here yet. Agentic workflows and complex automation. This is where the hype is thickest and the reality is thinnest.

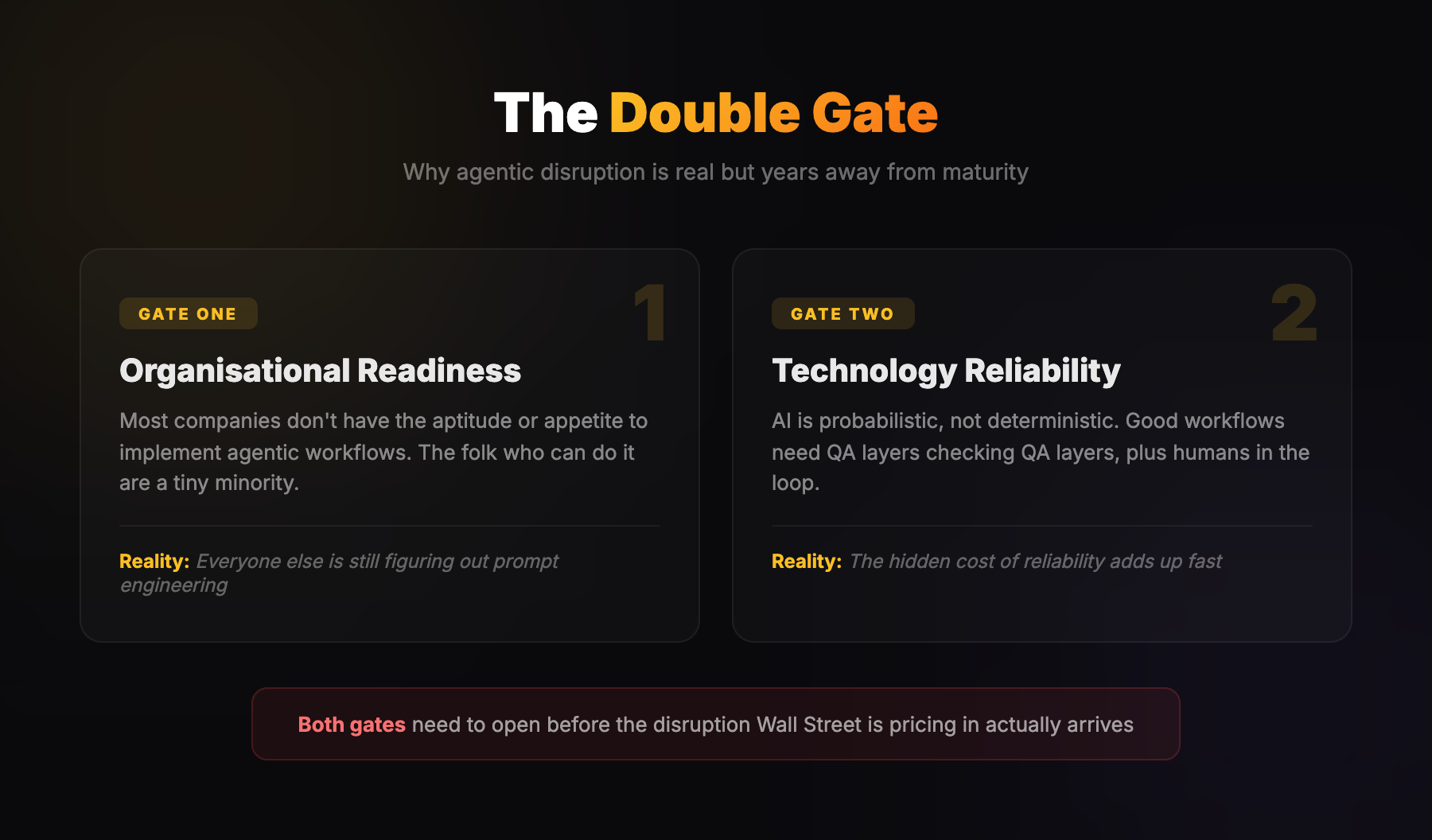

The tech is improving fast. But there's a double gate that nobody seems to be pricing in.

First gate: organisational readiness. Most companies don't have the aptitude or appetite to implement agentic workflows properly. The folk who can do it are a tiny minority. Everyone else is still figuring out prompt engineering (which is the bit that never gets discussed in the stock analyst reports).

Second gate: reliability. AI is probabilistic, not deterministic. Even good agentic workflows need multiple QA layers - often other AI agents checking the work - plus humans in the loop for final validation. That adds cost and complexity that isn't in the vibe coding narrative. When someone reckons they've "replaced a tool with an agent," they're usually not accounting for the QA infrastructure needed to make it production-grade.

I've seen this firsthand. A content creation engine that works brilliantly 90% of the time - then makes an unpredictable mistake because LLMs are probabilistic, not deterministic. You need a QA layer. Then you need a QA layer for the QA layer. Then you need a human to sanity-check the whole thing. The hidden cost of reliability adds up fast.

Both gates need to open before the disruption everyone's pricing in actually arrives. That's not next quarter.

Moated and adapting. Data-rich platforms with proprietary infrastructure. This is the category Wall Street is most wrong about.

You can't vibe-code a web crawl index. Ahrefs and Semrush sit on proprietary databases of billions of backlinks and SERP data, crawled continuously. ChatGPT can't give you accurate search volumes or current rankings because it doesn't crawl the web. Both platforms are adapting - Semrush launched Semrush One for tracking AI search visibility, Ahrefs launched Brand Radar. The AI SEO tools market is projected to reach $6 billion by 2035. These tools aren't dying. They're growing.

You can't vibe-code email deliverability infrastructure, ISP relationships, or DKIM compliance. Klaviyo's moat isn't its UI - it's deep e-commerce data integration and predictive intelligence trained on millions of purchase events. You can vibe-code a form that sends an email. You cannot vibe-code the infrastructure that ensures it actually lands in someone's inbox.

The Enterprise Moat Nobody Mentions

Someone replaced Loom with a vibe-coded internal tool. Works fine.

Until you need SOC 2 compliance. Or granular access controls. Or audit trails. Or enterprise-grade security permissions.

Can you replace some of the functionality of some SaaS tools? Yes. But if you're a mid-market or enterprise company and you need security and robustness, it's improbable that you're going to be allowed to do it (or that it's a good idea). Your CISO isn't signing off on a weekend vibe-coding project handling customer data.

Wall Street is pricing in disruption as though every customer can just vibe-code a replacement. In reality, only SMB and maybe lower mid-market can - and even then, most won't bother.

There's a reason Loom, Salesforce, and HubSpot all have enterprise tiers with dedicated security and compliance features. Those features aren't a nice-to-have - they're a procurement requirement. And procurement requirements don't care how good your vibe-coded alternative looks in a demo.

The market is pricing the entire customer base as at-risk when it's really the bottom tier. That's a significant misread.

The Messy Middle

The most interesting category is the one nobody can agree on. Marketing automation platforms like HubSpot, social media management tools like Sprout Social - these sit in a grey zone.

HubSpot is explicitly named by insiders as "sitting on top of the work" - its stock is down roughly 50% over the past year. The per-seat pricing model is under structural pressure as AI agents reduce headcount needs. But HubSpot's moat isn't the automation layer. It's the CRM data, the 1,500 app integrations, the deliverability infrastructure, the ecosystem. You can vibe-code a workflow. You cannot vibe-code ten years of contact data and domain reputation.

Social media tools are in a similar race. Hootsuite and Sprout Social are aggressively integrating AI - caption generation, auto-replies handling 80% of messages, sentiment analysis. New AI-native competitors like Enrich Labs claim to replace $9,000/month in tools and labour at $149/month. The scheduling and posting layer is easily replicated. The listening, analytics, and cross-platform intelligence layer is harder.

These tools' survival depends on how fast they shift from selling seats to selling outcomes, and how deeply they embed AI before someone vibe-codes a "good enough" replacement for their simpler users. That's a genuine race - but it's a multi-year one, not a quarterly cliff.

The Real Threat Isn't Vibe Coding

The actual competitive threat to incumbents isn't some bloke vibe-coding a replacement in his bedroom. It's AI-native competitors who are purpose-built and genuinely superior in specific use cases. Normal market dynamics, not an apocalypse.

Clay didn't replace anyone's CRM. It created a new category of data enrichment and workflow orchestration that wasn't economically viable before. ElevenLabs didn't replace a SaaS tool - it replaced production budgets and voice actor contracts. Cursor isn't replacing VS Code. Developers pay for both (which is pure market expansion, not replacement).

More net new categories are being created than old ones being cannibalised. That's the actual story. Wall Street is pricing in replacement risk when the real value creation is in expansion. The money is leaving incumbents and hasn't figured out where to reallocate yet - because the new categories are still forming.

Meanwhile, legacy players are being chipped away slowly but not collapsing. There's a massive repackaging of existing capability as "AI" happening across the industry (even when it isn't - slapping "AI-powered" on a feature that's been running for three years doesn't count). Some vendors are genuinely building AI features and functionality, but they're definitely not AI-first. And in certain categories, the AI-first players are having their lunch because they are genuinely superior. Data enrichment, outbound, and analysis are the clearest examples.

But the big incumbents - the HubSpots, the Salesforces - aren't facing an immediate existential threat from what I can see on the ground. They're being chipped at, not replaced.

What the Headcount Data Actually Shows

If these companies were truly under existential threat, you'd expect to see it in their hiring. Stocks can be driven by narrative. Headcount can't.

I pulled the employee growth data for the companies supposedly getting hammered by AI. The results are telling.

!Employee Growth vs Stock Panic

Duolingo is up 76% in two years. Datadog up 63%. Figma up 55%. Atlassian up 52%. HubSpot up 40%. These are companies growing aggressively whilst their stock prices crater - which suggests the drops are more about market sentiment than operational reality. Either that, or they're investing heavily to pivot towards AI themselves (which is still not the same as dying).

The only companies showing actual headcount declines are Chegg (-26%) and LegalZoom (-8%). Chegg is the clearest example of genuine AI disruption - homework help was always going to be obliterated by ChatGPT. Adobe is flat at 0%, which for a company of that size is notable stagnation.

But for the vast majority of the "SaaSpocalypse" poster children, the headcount tells a completely different story to the stock price. Wall Street is pricing in a future that the companies themselves clearly don't believe has arrived yet.

The automation and integration tools - the Zapier category - are the ones I reckon are most genuinely at risk. Those are thin workflow layers that folk can now build themselves. But the platforms with data moats, compliance requirements, and deep integrations? Their hiring data says they're not worried. And they're probably right.

The Timing Gap

Wall Street is correct about the direction. The capability advancement is real and accelerating. They're projecting forward and pricing in what they reckon is going to happen.

And they're right.

They're just years early.

The panic comes from conflating the maturity curve. Just because AI killed translation services doesn't mean it's killing HubSpot next week. Different moats, different complexity, different timelines.

What I see on the ground: early adoption, experimentation, net new categories forming, folk building narrow agents for specific use cases. What I don't see: mass replacement of core software platforms that justifies wiping out hundreds of billions in market cap today.

The irony is the panic itself might accelerate the outcome - forcing more capital into AI innovation, which speeds up the very disruption the market is pricing in. Self-fulfilling prophecy, just on a longer timeline than anyone's spreadsheet says.

The folk who can see which tools are actually vulnerable versus which ones are just caught in the crossfire of a broad-brush narrative - those are the ones making better stack decisions right now.

Everyone else is just reading headlines...

Frequently Asked Questions

Is the SaaSpocalypse actually happening?

Partly. Basic content tools, simple workflow layers, and landing page builders are genuinely exposed - their core value is a UI sitting on top of something AI can now do natively. But the panic about SaaS broadly is overblown. Nobody I work with is trying to replace HubSpot or Salesforce internally. Folk are building narrow tools for workflows that were never software to begin with.

Which SaaS categories are most at risk from AI?

The most exposed are thin workflow and automation layers - the Zapier category - plus basic content creation tools and landing page builders. If your core value is a UI wrapper around something AI does natively, you are in trouble. Data-rich platforms with proprietary infrastructure (like Ahrefs, Klaviyo, or Semrush) are far more protected.

Why does headcount data contradict the stock market narrative?

Companies supposedly being hammered by AI - HubSpot, Figma, Atlassian, Datadog - are all growing headcount aggressively whilst their stock prices crater. That suggests the drops are driven by market sentiment, not operational reality. The only companies showing actual headcount declines are clear-cut cases like Chegg, where AI directly replaces the core product.

What is the double gate holding back agentic AI disruption?

First gate: organisational readiness. Most companies do not have the aptitude or appetite to implement agentic workflows properly. Second gate: reliability. AI is probabilistic, not deterministic - you need QA layers, often other agents checking the work, plus humans for final validation. Both gates need to open before the disruption Wall Street is pricing in actually arrives.

What is the real competitive threat to incumbent SaaS?

It is not some bloke vibe-coding a replacement in his bedroom. It is AI-native competitors who are purpose-built and genuinely superior in specific use cases - Clay, ElevenLabs, Cursor. More net new categories are being created than old ones being cannibalised. The actual story is market expansion, not replacement.

Oren Greenberg

GTM Engineering Advisor · 21+ years in growth & GTM

Oren advises B2B SaaS companies on go-to-market engineering, growth strategy, and AI-driven marketing.

Connect on LinkedIn