Growth Hacking Course

Your GTM Platform's AI Features Were Designed to Keep You Subscribed, Not Win You Pipeline

By

June 27, 2026

87% of B2B marketers now use generative AI in at least one workflow [arisegtm.com, 2026]. Only around 6% of organisations are extracting bottom-line value from it [arisegtm.com, 2026].

That gap is not an adoption problem. It's a design problem - and the design was never yours to control.

The AI features embedded in your GTM platforms were architected to reduce your churn probability, not to maximise your pipeline conversion. Understanding the difference between those 2 objectives is the most commercially important question a CRO or VP Revenue can ask right now.

The retention motive is the product roadmap

Every major GTM platform - Salesforce, HubSpot, Outreach, Gong, 6sense - has spent the last 18 months announcing AI features. The pattern is recognisable: capability launches tied to pricing tier upgrades, AI bundled into enterprise seats, product marketing that equates feature access with competitive advantage.

That's not cynicism. That's product strategy, and it's entirely rational from the vendor's perspective.

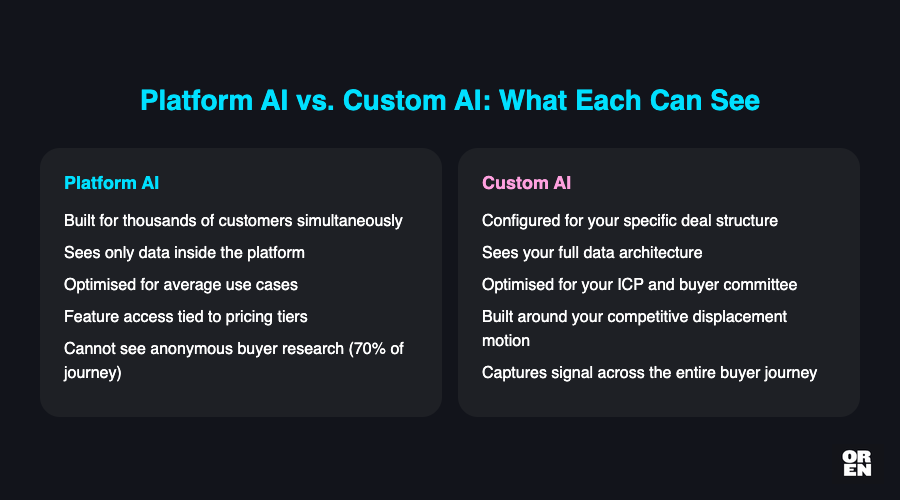

A platform serving thousands of B2B companies simultaneously cannot build AI optimised for your specific deal structure, your buyer committee dynamics, your competitive displacement motion, or the particular way your ICP researches before they ever speak to sales. The average B2B buyer spends 70% of their journey researching anonymously before reaching out [WBResearch, 2026]. Platform AI cannot see that journey the way a system built around your specific data architecture can. It sees the data you've chosen to put inside the platform - which is, by definition, a fraction of the signal that matters.

The commercial ceiling is structural. What a vendor can profitably build for thousands of customers simultaneously is categorically different from what's possible when AI is configured for a single company's specific motion. No amount of disciplined prompting closes that distance, because the constraint isn't how you use the feature. It's what the feature was designed to do.

"Almost everyone has adopted AI. Almost nobody has gained an edge from it. That gap is the real story of 2026." - Paul Sullivan, Arise GTM

The pricing signal nobody is reading

When Salesforce introduced Einstein Copilot and HubSpot rolled out its AI suite, both tied the deepest functionality to higher pricing tiers. This is not coincidental.

AI features are the most defensible mechanism for per-seat price increases the SaaS industry has seen in a decade. The feature exists, in part, to justify the renewal conversation and to make the cost of switching feel larger.

B2B companies already rely on an average of 15+ dedicated GTM tools spanning sales intelligence, CRM, marketing automation, and ABM platforms [HG Insights, 2026]. Each of those vendors is now adding AI capability. Each is pricing it upward. The aggregate effect on a mid-market GTM budget - £10M to £100M ARR companies running full stacks - is significant, and the value attribution is almost impossible to isolate cleanly enough to present to a board.

This is the pain point I hear repeatedly from CROs and VPs Revenue in the UK and Western Europe: "We're spending but I can't prove the value."

The inability to prove value is not a measurement failure. It's a consequence of buying AI features designed to deepen platform stickiness rather than produce a measurable, attributable commercial output.

I've written about the architecture problem sitting underneath this in Your GTM Stack Is an Expensive Mess. AI-Native Companies Figured Out Why. - the short version is that decades of buying disconnected point solutions created Frankenstacks where data never properly connects, and AI features layered on top of a Frankenstack inherit all of its structural weaknesses.

What 'custom' actually means here

The alternative to platform AI features is not vibe coding your own CRM. I want to be precise about this, because the democratisation narrative has made the options seem simpler than they are.

AI coding tools like Claude Code and Cursor are genuinely useful for ad-hoc tasks. But the hidden costs of maintaining custom-built systems - debugging, updating models, managing integrations as third-party APIs change - make the "just build it yourself" argument questionable for anything mission-critical. The SaaSpocalypse narrative that 35% of enterprises are replacing core SaaS with custom builds is also technically misleading - the tools being replaced are integration layers like Zapier, not CRMs or data infrastructure with proprietary network effects.

Custom AI capability, in the context of GTM, means something specific and more modest: AI-powered workflows and systems that sit alongside your existing platforms, trained on your data, configured around your commercial motion, and owned by you rather than rented from a vendor at an increasing price per seat.

The distinction matters practically. A custom signal-to-sequence workflow that pulls anonymous intent data from your specific target accounts, cross-references it against your historical win/loss data, and surfaces prioritised outreach triggers is not something any platform vendor will build for you. It requires knowing your ICP at a level of specificity that is commercially unviable to productise. When Notion launched their AI-native product, they had approximately 2 million people on their waiting list within a couple of weeks [Máire O'Herlihy, OpenAI GTM team, 2025] - that scale of demand is precisely why Notion's AI is built for the broadest possible use case, not yours.

The audit you should run before the next renewal

Before you sign the next platform AI upgrade, run a simple stress-test against your actual commercial motion. Four questions.

Whose data trained this feature? Platform AI is trained on aggregate customer data, which means it reflects average patterns across industries, deal sizes, and buyer types that may have nothing to do with your segment. Ask the vendor explicitly what data underpins the model and whether it can be fine-tuned on your historical data. Most cannot.

What is the feature optimising for? Lead scoring features optimise for engagement signals that correlate with conversion across the vendor's entire customer base. Your conversion drivers may be entirely different - a specific sequence of content consumption, a particular firmographic combination, a competitive displacement trigger. If the optimisation objective doesn't match your motion, the output is noise dressed as signal.

Can you measure it independently? If the AI feature lives entirely inside the platform and its output is only measurable using the platform's own reporting, you have a measurement dependency that makes objective evaluation structurally impossible. This is not an accident.

What happens to this capability if you churn? It disappears. Any GTM edge you built on top of a vendor's AI feature is not yours - it's a licence you're renting. Custom-built capability compounds over time as your data improves and your workflows mature. Platform AI capability resets to zero the moment the contract ends.

The 6% and what they are actually doing

The 6% of organisations extracting bottom-line value from AI are not using better tools [arisegtm.com, 2026]. They're using AI differently - with specific workflows built around specific commercial outcomes, with human judgment retained at the decision points that matter, and with measurement frameworks that connect AI activity to revenue rather than to activity metrics.

"AI-native, human-first is not a slogan; it is the difference between the 6% who get value and the rest." - Paul Sullivan, Arise GTM

The human judgment point is not peripheral. 67% of B2B buyers say they can spot unedited AI content, and 58% say unedited AI content reduces their trust in the brand that published it [arisegtm.com, 2026]. The AI features your platform vendors are selling you are, in many cases, producing exactly this output - generic, unedited, trust-eroding content at scale.

81% of B2B buyers who are happy with AI-assisted content require it to be accurate, specific, and carry original thinking [arisegtm.com, 2026]. Specificity and original thinking are not things a platform AI feature can supply. They come from your commercial context, your category expertise, your understanding of your buyer - none of which lives inside the vendor's model.

This connects to a broader point about AI fluency. Counting AI tool licences activated is a vanity metric that measures spending, not capability. Most teams are stuck at the prompt-engineering stage of AI adoption whilst reporting to their boards that they're deploying AI across the revenue function. The gap between licence activation and genuine workflow transformation is where most GTM AI spend disappears.

The build vs. extend decision

The practical question for a CRO or VP Revenue is not "should we use AI?" - that's settled. It's "where does the platform's ceiling sit relative to our commercial ambition, and what does it cost us to stay below that ceiling?"

For most mid-market B2B SaaS and FinTech companies in the £10M-£100M ARR range, the ceiling is already visible. Platform AI features handle the generic cases adequately. The specific cases - the ones that actually differentiate your pipeline generation from your competitors' - are precisely what the platform cannot and will not build, because building them for you would make the feature commercially unviable to offer to everyone else.

The decision to extend platform AI versus commission custom capability is not a technology decision. It's a strategic question about whether your GTM motion is generic enough to be served by tools built for thousands of simultaneous customers, or specific enough to warrant building for your exact commercial context. For companies with a defined ICP, a repeatable sales motion, and a competitive context that requires genuine differentiation, the answer is usually that the platform ceiling is lower than the vendor's marketing suggests.

If you're working through this decision, the growth audit framework I use with clients starts with the commercial motion before it touches tooling - because buying AI capability before you've defined what you're trying to achieve with it is how you end up with an expensive stack and a board presentation you cannot defend.

The vendors are not your adversaries. But their product roadmap serves their retention economics first. Knowing that, and building your AI capability strategy around it, is the starting point for being in the 6% rather than the 94%.